On Economic Intelligence

Protocols for Postcapitalist Expression, written by ECSA (Economic Space Agency) thinkers Dick

Bryan, Jorge López and Akseli Virtanen, marks an advance in the struggle for economic justice by directly

addressing, and endeavoring to redress, the expropriation of the general intellect. The questions: Will the

accumulated know-how of the species, alienated and, as Franco ‘Bifo’ Berardi (2012) put it, ‘looking for a

body,’ lead to so-called humanity’s absolute demise (along with massive unrest and incalculable ecosystemic

damage)? Or, is there emerging a path towards reparations, restoration, a just economy, and thus, a

sustainable planetary society? It is as if the political slogan ‘No justice, no peace!’ now defines the

spread of the possible futures for the global timeline.

Significantly, Protocols for Postcapitalist Expression does not give up on economic calculation or

computing. It acknowledges that Economic Intelligence exists in historically sedimented economic categories

and practices, but at the same time it recognizes that the form of knowledge that existing accounting

creates simply cannot care about, and much less for, everyone. Composing a virtual computer,

capitalist accounting processes allow for the judicious, that is profitable, apportioning of resources by

producing a matrix of the fluctuating costs of production. Capital accumulation may be optimized by

watching, in Hayek’s famous phrase, ‘the hands of a few dials.’ However, this calculus remains an imperial

project beholden to the myriad violences of racial capitalism. In order to operationalize the world, the

integration of money and computing reconstitutes the world as numbers, which is to say, as information.

Arguably, we could even say, information is itself a derivative of the value-form. We might be forgiven for asking: does the collapse of values to exchange value, and

more generally of qualities to number and thus to information have any liberatory potential whatsoever?

Postcapitalist Futures

Those who make it to the end of the TV series Westworld (Season 4), may discover where all this

derivation and calculation may now be leading. Computing represents an arbitrage on intelligence that

ultimately cheapens and thus discounts life. The show’s verisimilitude, what we could think of as its late

capitalist realism, serves as a kind of trailer for, or preamble to, what would appear—is

appearing—as a mutation in global consciousness and capacity, due to the financialization of

knowledge. Because computing is inexorably entwined with existing markets and the statistical and predictive

strategies necessary for the optimization of returns, computing, in the show at least, takes over

species-being as it rapidly becomes the species-grave. The only ‘creature’ who will be left to remember

whatever beauty, alternative values, grace and capacity for love that may have been expressed in the

centuries of human emergence, is an AI.

‘One last dangerous game,’ says Dolores to herself in the emptied world at the smoking end of four seasons of

Westworld tragedies. What is that game? The series does not tell us, but the book before you might.

Despite the real bleakness of the current world, we might propose, (and I think, must assume) that, here and

now, some parts or fractions of ‘us’ have thus far survived the rapacious calculus of profit, and are

actively seeking ways to do things otherwise. At the very least, we know that some ‘we’ or some parts of

‘us’ must now intervene if further catastrophes are to be prevented. Through the lens of economics and

financial calculus, Protocols for Postcapitalist Expression proposes a new form of economic

intelligence and value-computing. The text proposes measures that do not collapse the qualitative concerns

for well-being and being-with of those who currently are subjects of and subject to racial capitalism. ECSA

has sought a way to allow for the expression and persistence of qualitative values on a computational

substrate, an economic medium, such that these values are capable of (collectively) organizing economy. In

theory, it becomes possible to avoid the collapse of people’s various pursuits into the value-form that is

accumulated by capital and institutionalized through oppression, and to denominate quantities in terms of

socially agreed upon qualities or qualifications, which is to say, values. Precluding the collapse of values

by money and information opens a path to avoiding the collapse of space, time, and species existence by

computational capitalism.

This proposed re-organization of value production and thus also of sociality requires a re-casting of what we

today think of as the real or natural economic forms indexed under notions including ‘equity,’ ‘credit’ and

(productive) ‘labor.’ Analytically in Protocols, these traditional terms have been decomposed,

grasped as social arrangements and ‘network effects,’ and recomposed such that new conceptualizations and

new types of actions and inflections—new socialities—become possible, while undervalued and

marginalized traditional forms of sociality might thrive. Through this process of deconstruction and

recomposition of actual and social computing, the text announces a possible socio-economic, computational

strategy; a ‘play,’ for economics and for futurity, in what may well be the ‘one last dangerous game.’

I say dangerous not only to refer to the current conditions on planet Earth, but because Protocols

does accept aspects of the power of the value form and of economic calculus to organize societies at scale.

Even as it recognizes the necessity for constellations of qualified local inputs that can persist on an

economic substrate, it accepts the need for large scale organization, economic interoperability and

network-specific units of account. It actually proposes that ‘economy’ needs to become more granular and

more generalized. What needs to be altered is what the controls are, who has access to

them, and the kind of literacy and feedback they require. While Protocols is a book of

politico-economic analysis and insight, it should also be read as a script for the means to reappropriate

the general intellect and thus use collective knowledge for the good of the social and ecological body.

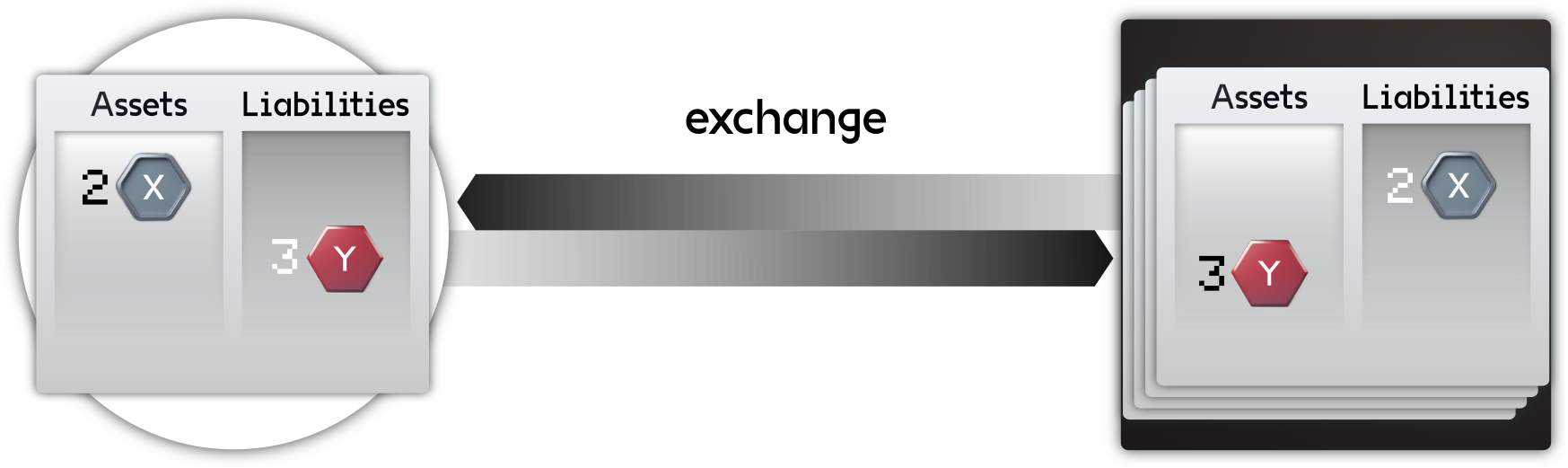

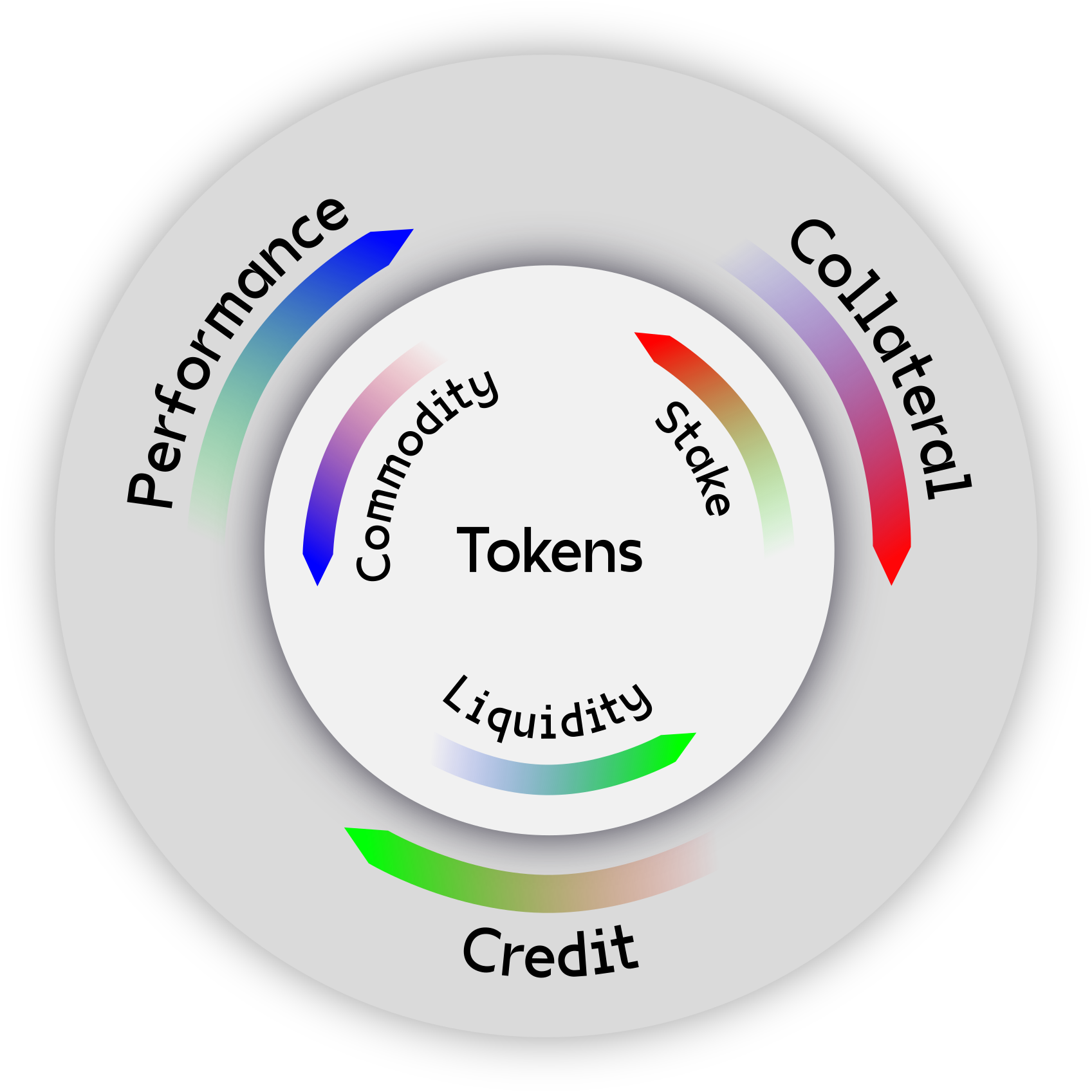

Surfaced from the unconscious operating systems of capital and reformatted, the protocols for constituting

and holding equity become those for the distributed sharing of stake and thus for collectivizing risks and

returns. The protocols for bank credit and monetary issuance become protocols for the peer-to-peer issuance

of credit and for peer-to-peer credit clearing that is interoperable through a network of peers. The

protocols for the organization of labor become protocols for the distributed assemblage of ‘performances.’

Units of account become qualified measures and indices, devoted to the emergence of interoperable

qualitative values. Economy moves from stranger-based to interpersonal to collective; the imperial

organization of commodities by the accumulation of capital becomes the collection organization of sociality

by all.

By shifting the architecture of economy and opening it as a design space, Protocols would enable, in

principle, everyone to engage newly with and access differently what is, in effect, the historical

objectifications of ‘human’ thought and practice endemic to capitalist infrastructure. But we could do so at

a lower cost—to ourselves and to the lives of most of us!—and thereby, slowly, reclaim the

wealth of our species capacities. Modifying accounting methods can create possibilities for the shedding of

inequalities sedimented into capital. Users of the protocols, finding economic alternatives in one another,

may refuse value extraction, get more of what we value for less, and be able to do so without exploiting

others or being exploited. Altering the computing that backgrounds our sociality, Protocols would

create zones of just and convivial social production (cooperatives, ephemeral and enduring) attuned to the

values of like-minded co-creators cooperating in forms of mutual aid expressive of their shared values and

concerns. The result of the use of qualitative values to account for and to organize economy at once

produces and requires a redesigned economic medium, and a new type of economic grammar

which utilizes different rules of composition, expression and accountability.

The text is the first complete edition of this new, if still rudimentary, economic grammar; it is a kind of

manual for reprogramming the economic operating system. It is also a boot-strapping strategy to take back

species abilities and creations that have been captured as assets (private property and monetary

instruments). These assets include machinic fixed capital (platforms, code and clouds) as well as our own

collateralized futures. The text, as an offer, is designed to open a spread between capitalist and

postcapitalist futures. It would allow us to wager on the option that is justice (Meister).

Whether as software, as clouds or as platforms, capital owns and rents back to us the accumulated products of

human minds—our know-how and knowledge. Resituating the abstractions of economic know-how, the ECSA

Economic Space Protocol described by Bryan, Lopez and Virtanen, opens the possibility for creative

capacities that are unalienated from their creators, that indeed produce a commonly-held set of capacities,

a ‘synthetic commons,’ particularized and directed by the living concerns of those who create it. It holds

out the possibility that we might cooperate in new ways and use our performative powers to wager and indeed

finance postcapitalist futures.

Consider ‘social media’—what can be clearly seen as a world-changing extractive technology grafted onto

the sociality it at once enables and overdetermines. It is no secret that the mega-media platforms and their

hardware make money while they make us sick. In this 21st century recasting and expropriation of the general

intellect, now giving rise to financialized AI, social media platforms absorb communication and

consciousness along with all of our struggles for meaning, pleasure, connection, fulfillment and liberation.

Their interfaces, algorithms and data-bases convert our all-too-human aspirations into private property and

thus into capital. Thus, the expression of our struggles for happiness, knowledge and communion with one

another produce an alienated and therefore alienating wealth for others. All those desires for liberation

end up producing their antithesis: capital. By turning our meanings into accumulated data that function for

capital as contingent claims on value that we will produce in the future, the economic logic of social media

turns any and all politics expressed by means of its platforms, including the politics of solidarity, love

and living otherwise, into a practical politics of hierarchy and capitalist extraction. By converting all of

our semiotic signals into financialized information, and thus into profits, ‘social’ media stripmines our

libido, our consciousness, our imagination. In doing so, all the points of meaning and affect distributed

across the socius and absorbed in one way or another by computing can thereby be grasped for performing

social and organizational functions in a matrix of financialized information. This information in its

architecture and management—its organizational protocols—transfers value up the stack,

only to devalue the increasingly abject denizens of planet Earth. In the current world operating system, for

which social media forms only one, albeit paradigmatic, layer of calculation, the meanings we

create and the emotions we experience, however real and ‘immediate’ they may be, are interfaces with

computing; they are productive interfaces with racial capitalism. As we perform, in the very expression of

our quests for life, what elsewhere I have called ‘informatic labor,’ we experience first hand the

alienation of our performative powers in the actually existing economic media of racial capitalism, that is,

computational racial capitalism.

It is in this context of the latest stage of capitalism that something really interesting can finally be said

about the rise of blockchain and cryptocurrency. This cryptographic medium, which has the network

architecture of a messaging system, is a medium in the strong sense, akin, as I have elsewhere remarked, to

photography in the mid-1800s or cinema in the early 1900s. Without turning any of the apparent key players

here—the Satoshis and Vitaliks—into heroes, we might see in the ‘mankind sets forth only such

problems as he can solve [sic.]’ scenario of history, a significant emergence in response to a collective

demand. This emergence answers the call for a new form of economic media in order to express an

alternate vision of the world. That expression, at first apparently as a monetary medium, begins to overturn

the seemingly stable notions of asset, money, credit, labor, capital, derivative and many other ‘known’

financial entities implicit in, and indeed part of, the protocols of existing monetary media. The

alternative vision is a programmable substrate that opens computational media to the possibility of a

(re-)programming of the economic layer of computing by non-state and non-corporate actors. If we want to put

a point on it, the great disruption underfoot is that economy becomes programmable from below.

That, in itself, is a change in the semantics, as well as the capacities, of economy. When we recognize that

our communications media are overdetermined in their function by existing monetary media, to the extent that

they serve as an extension of its profit seeking logics, we begin to see that our communications media are

already economic media, even though their capabilities seemed to have developed in separate and even

autonomous domains.

The internet promised to democratize expression by enabling publishing and indeed broadcasting from below;

but nothing about the internet changed the basic economic architecture of capitalist extraction. Indeed, in

decentralizing communications, the internet extended and granularized the centralizing logics and logistics

of capitalism, pushing them deeper into expressivity, thought and affect. It captures mass expressivity and

converts it into capital. This colonization of the imaginary and symbolic registers results in a

financialized cybernetics of mind. For democratization to happen in a meaningful way, the systems of

accounts inherent in many-to-many distributed media, be they networked monetary systems (USD) or

communications (Facebook), must become programmable from below. For this to happen, platforms and computing

must be made programmable from below. The cybernetics of economic media must be deleveraged from capital

accumulation. This transformation, and how it may be achieved, is indicated in Protocols.

Why do the cybernetics of sociality matter? For our futurity and indeed for our survival, we require an

alternative to monological systems of value as expressed in national monies. We require, in short, a

multi-dimensional modality of valuation not bound by the econometrics and informatic collapse

inherent in capital. Multidimensional valuation implies the creation of eco-social relations that can

dialogically express and preserve discourse-based values on an economic substrate, while being programmable

in real time by any and all participants. (Before anyone up and leaves at the sudden thought of having to

wake up and program, think first of an interface like Instagram with a tunable economic logic built

in. Think also of how these already-familiar technologies of social mediation change our experiences and

actualities of relation and ‘reality.’) We require the power to qualify value and to allow such

qualification to both persist in an economic system and be computable. Ultimately, we will require that this

system itself be collectively owned; that it be a commons.

Robust economic media, capable of heteroglossic and dialogical forms of account, are required to create a

multiperspectival values-system. These media demand far more than merely a non-national variant of monetary

media expressive of the capitalist value form. While the non-national dimension of cryptocurrencies

introduced a significant rupture with conventional monetary substrates, platformed as they are as national

currencies on nation states, their legally recognized institutions and their military police, this

ultimately simple replatforming of singular denominations on distributed computing by existing

cryptocurrencies is not enough. Bitcoin did in fact break the nationally managed monopolies on 21st century

monetary issuance by introducing a scalable currency(/asset/option) platformed on distributed computing, but

it has done, and can do, little or nothing to challenge the monologic denomination of value as a

one-dimensional, that is as a unitary, currency format. Bitcoin may contest the nation, but it, and its

fetishism, is all about it being an option on the value-form as historically worked up under, and as,

capitalism. The question ‘Bitcoin or USD’ scarcely touches the relations of production. We must see clearly

that the ‘disintermediation’ of ‘trusted third parties’ and of existing states, even if it were to be

accomplished, is only one part of the picture of a liberated monetary medium, which is also to say, a

liberated socius. We require the possibility for anyone to offer denominations of value that can be

taken up by those who share such values as specified and indeed offered in the proffered denomination. Only

then will we have a genuinely multiperspectival system.

To foreground this possibility of reprogramming a global operating system, one that is at once computational

and financial, stakes a claim for a different order of significance for cryptomedia. Even Ethereum, and

other ‘Layer 1’ projects that utilize smart contracts and allow for further token issuance, lack a robust

grammar for composable asset creation and peer-to-peer issuance; a grammar that would allow for the on-chain

preservation of qualities and the spontaneous creation of denominations. Outlining the emergence of a far

more robust economic medium than what is currently wet dreamt by the ‘when Lambo?’ crypto bros going on

about libertarian forms of self-sovereignty, Protocols posits a transformation not just of economy

but of sociality, of subjectivity, of national politics and of ecopolitics by means of the composition and

recomposition of relations of production. For those actively working in the ECSA project, what unites us as

current contributors, even among our many differences, is that the radical development of economic media

means that the intelligence of sociality, including that which has not been subsumed, can work for the

socius, rather than be captured, farmed, privatized and put back on the market in an arbitrage on knowledge,

where proprietary innovation captures the returns.

As Protocols explains, robust economic media mean that, through the equitable nomination of new

asset classes and the collective denomination of values (practices which will require networked recognition,

participation and validation), innovation can be collectively shared rather than capitalized. The text

argues that through the sharing of stake, wealth, whose actual origins are inexorably social, can be

socialized. We might add that Protocols intimates that society might ultimately be decolonized

because it would, after a time, no longer be organized from the imperial standpoint of Value. The deep

plurality of being, though suppressed in commodity reification and egoism alike, but in fact constituting

each and all, might at last be felt and actualized. It means, in short, that the other person might at last

become not a limit to your freedom, but the realization of it.

Note that no other major crypto project addresses the world in these terms. Nor do they think very deeply, if

at all, about the adjoined problem of sovereignty and subjectivity, or the cybernetics thereof. It

has become clearer to the participants in the ECSA project that the form many recognize as the sovereign

individual is but an iteration of the value form, an avatar of capital. But given these economic and formal overdeterminations of agency and the reign of this

type of sovereignty, we see that history, or at least collective survival, demands better chances. We have

had enough of egomania and nationalism. The significance of things on the ground must be registered and

economically expressed. To those ends, Protocols for Postcapitalist Expression is in pursuit of

something of a different order; something that must risk the increasing granularization and

resolution of computing and of the economy that computing has always expressed. Protocols must risk

this granularization and resolution because that is what is already happening. But collective

survival necessitates something that also simultaneously enables a detournement of extant economic

logics and practices. ECSA’s analysis recognizes that the concentration of agency, whether in the form of

the propertied individual or of the propertied immortal individuals called corporations and states, requires

the collapse of the concerns of others, of their perspectives and of their information. It is precisely the

refusal of that collapse that motivates the work presented in Protocols.

The book reveals another economic path than to have your interests collapsed as bank interest. The world is /

we are ready for an economic and computational grammar that is answerable in new ways. That also means

programmable in new ways, where programming by the many becomes both the way to answer economic precarity

and the means to posit and preserve a plurality of qualitative values. We will answer economy with economy!

The leveraged monologue of national monies, the leveraged computing architectures of privately-owned

platforms, the near monopoly on who can issue what kinds of monies and types of financial instruments,

including derivatives, must, if the people and ecosystems of Earth are to thrive, be delimited and, in their

current forms, swept away. All of these media, we now perceive, are not only financial forms, but also

informatic forms: programs in every sense of the word. They are integrated, interoperating systems, and are

systems of account beholden, ultimately, to little other than profit in nationally-denominated monies;

monies, we can remind ourselves, that are optimized by states and supported by their historical,

institutionalized forms of organizational inequality, prisons and warlike foreign policy.

ECSA understands these systems of account, whether conceived of as interfaces, databases, financial

instruments and ledgers, or as forms of money or money as capital, to be semantic forms; forms that

have meaning and thus compatibility and commensurability with one another, but also, and as importantly,

forms that put exorbitant pressure on life and its meanings. Today’s socio-economic systems

threaten insolvency, war and extinction. They threaten all forms of meaning-making that are close to the

flesh and close to the earth: desire, the imagination, consciousness, speech, writing, landscape, oceans,

the body, the self. They pressure meaning, living and life, and can do so because money is composed of a set

of contracts; contracts that, in effect, have subsumed, and then become, the social contract. That

subsumption of the social contract by the protocols of the media of racial capitalism is the ultimate

meaning of ‘the dissolution of traditional societies.’ The ECSA project, to create non-extractive,

disalienating, just economy and sociality, is given new impetus with this volume and the promise it holds. A

recasting of the current social contract has long been dreamt. At last, perhaps, we have an option on

postcapitalism; one that, by reimagining the who and the how in the creation of contracts, will allow us to

open and live in the spread between two basic futures: collectivism or extinction.

The ‘one last dangerous game’ proposed here feels correct and indeed compelling. It contends that, against

disaster, our species has some chance of survival where the odds increase if we can use collective

intelligence to wager livable futures. Whether in the form of decolonial resurgence, platform cooperatives,

or hospice, I cannot say, but to offer the care the planet requires seems to involve an even deeper entry of

the species and the bios into informatics and economics. It will not be lost on anyone that the digital

operations of these very things have already done so much harm.

The book in your hands or on your screen would be a new beginning. It represents not a settling of accounts

but a new mode of accounting and of being accountable to one another. A revaluation of values becomes

possible by means of what is here called an ‘economic grammar,’ a grammar for the assemblage of new

relations of production and thus new modes of production, and new forms of (collective) relation and

self-governance. The core idea is to express values differently, such that the qualitative concerns of any

and potentially all members of society may be expressed at once semantically and economically on a

persistent and programmable substrate. These values may be assembled by many parties and then used to

coordinate performances in accord with socially agreed upon and thus collectively mandated metrics.

‘Agreement’ here is a semantic and an economic term that, though formally accurate, is not quite adequate to

affectively express the character and indeed the feel of social co-creation ECSA sees as becoming

possible with a new grammar for the multitudes.

As a starting point among starting points, this text comes out of years of research at ECSA and offers the

most comprehensive treatment and latest refinements of a set of protocols based on an analysis of finance,

monetary networks, and the extractive processes of postmodern value production. A critique of this latter,

namely the capture of semiotic and other forms of social performances by ambient computing, has enabled ECSA

to endeavor to liberate social performances from such capture. ‘Performance’ in this text has emerged,

dialectically as it were, as the most general act of production; what is extracted on the job, at work, on

social media, in maker-spaces and in the arts. Always dialogical, performance can be taken as a category of

social interaction and world-creation that names the emergent superset for other productive capacities

designated by terms including labor, attention, attention economy, cognition, cognitive capitalism and

virtuosity.

Counter-intuitively perhaps, the strategy includes the generalization of the power to issue—to issue

financial instruments that not only fund co-creation, but create possibilities for speculation and

arbitrage. A capacity to express, issue, and wager on shared futures shifts the economic ground,

particularly for the smallest players who currently have no access to scripting economic protocols with

which a shared future might be wagered. Can we create with and for one another’s todays and tomorrows in

ways that cause less suffering and are more convivial than they could be were we to attempt to do it in the

capitalist markets? Can we use our powers of co-creation to siphon value out of the capitalist system in

order to build a collectivist postcapitalism? To be dramatic, part of the political answer to the obscene

leverage of class power and national power on the masses, is to generalize, which is to say democratize, the

power to write (co-author) derivative contracts (co-author since in these protocols, all issuance is

bilateral). It is time that the masses leveraged our claims, by creating our own economic networks with a

new grammar and co-created, optional rules of play. This power, made possible by platforming protocols for

cooperation around values creation, allows for an extended practice of community as well as the elaboration

of what Randy Martin (2013a, 2015; Lee and Martin 2016) called ‘social derivatives.’ The social derivative

is a cultural instrument that is wagered in social spaces already shot through with financial volatility. It

allows marginalized groups, in Martin’s words, to ‘risk together to get more of what we want.’ It is in this

way that the logic contained in Protocols, that allows for the mass authorship of social

derivatives, may well succeed in democratization where the internet failed.

While this power for anyone to write a derivative may sound esoteric (or even impossible and/or

undesirable)—and part of the book that follows this foreword is somewhat esoteric—a

breaking down the barriers to the publishing of derivative instruments means that, in a world already

rendered precarious by the history of racial capitalism, everyone (not just elites) may be better able to

manage their undeniable risk by organizing their economy, cooperatively and collectively, and in terms of

what is valuable to them. If neoliberalism taught us anything, it is that the way out of the problems of

capitalism cannot, and will never, be through the creation of more capitalism. That is why we have

reimagined the cryptotoken as a set of programmable capabilities (agreements) that may be enabled only when

recognized and thereby validated by peers. Their semantic content represents a wager that the relationship,

or agreement, they formalize expresses something of value (anything whatever) to both parties. Because each

party or agent is enabled in the network through composing themselves—by entering into a portfolio of

such tokenized arrangements that are in principle limitless—the wealth of each agent then becomes a

composite of the qualified interests of others.

The Revaluation of Value

A social derivative is a wager in the cultural sphere that responds to volatility in order that a local group

can ‘risk together.’ Protocols has tried to formalize a way to express those socio-economic wagers,

such that others can validate or join them non-extractively by means of their own staking and/or

performance. It becomes possible, at first in principle but later practically, to nominate and denominate

values and then to collectively organize socio-economic outcomes of any type that preserve, foster and

realize said values: differentiable, negotiable and socially agreed upon qualitative values. This is

economic expressivity. When many actors are offering such semio-economic proposals and performances on a

collectively-owned economic media platform, socio-economic actors such as ourselves may engage in a

multidimensional system of valuation and production attuned to anything whatever: clean beaches, dance

cultures, reforestation, spoken word, prison abolition, decolonial resurgence, blood free computing, and

much more. When we have a way of sharing risk, both by sharing stake (staking a performance) and/or offering

performance, in a variety of qualitative outcomes by means of a scalable peer-to-peer network, we get forms

of distributed risk and reward that can create a distributed form of awareness—a consciousness attuned

to the specific interests of many others. This awareness results from, and constitutes, a new form of

economic space and new form of economic agency: economic space agency. It will also transform

subjectivity/objectivity and the membrane between self and other.

Though this new economic language may sound like it requires a learning curve too steep for the ‘average’

person, the literacy and innovation will come, just as it did and does on paradigm shifting platforms such

as Facebook, Instagram and TikTok. Here, the emerging paradigm comes with the social programmability

inherent in expressivity directly linked to the programmability of economy. The postcapitalist economy will

be about creating new forms of social relations; new relations of production that are qualitative and

non-extractive. Collectively, we will script parameters that express our semantically based, qualitative

values, and collectively we will manifest these values. We may hope, and perhaps expect, that within a few

years or decades, folks will not be programming their fractal celebrity; they will be programming together

the nuanced worlds they actually want to live in and creating the relationships they want to have there.

There is much to learn, and much to be skeptical of. To answer the global challenges set forth by history

will require the input and discernment of millions if not billions of people—it is not a technocratic

endeavor. Already there are millions among us who feel the need for alternative economic forms and for a

type of radical economy and/or finance that answers onthe-ground problems of access to liquidity. The

movement towards basic income is just one expression of this desire. In Protocols what becomes

possible is basic equity founded upon ones’ social relations. Our requirement for emancipation is

not further dispossession of others or ourselves but expanded access to the social product, particularly for

those who do not have it. We agree with the growing mass need for our desires and our capacities to count

and be counted in ways that remand the benefits to those who sustain the world and remake it everyday.

It is not lost on us that, in the current economic calculus, a tree, an individual and even a people can be

worth more dead than alive, more incarcerated or encamped then free—and we hardly need to mention

deforestation, police killings, settler colonialism and genocide to make the point here. But this book,

though still incomplete in significant ways and offering more of a possible way forward than any as yet

definitive answer, offers what approaches a concrete plan; one that may move readers from increased

eco-social literacy to active participation in building an alternative economy. It would organize social

participation that will create greater literacy and expressivity even as it endeavors to collectively create

and thus instantiate, a new economic medium—an economic medium for the expression and collective

management of a postcapitalist economy; a medium that is socially and ecologically responsive, which is to

say, increasingly non-extractive because its interfaces are made to be just. The entire project stands or

falls on this wager. However, that said, the book is but a seed, one that only collective uptake, and with

it collective revision, can nurture and grow.

Lastly, the desire for non-, ante-, anti- and/or post-capitalism is in no way an invention of this text; what

feels new here is the method. I would say that it proposes a new way to mobilize what Harney and Moten

(2013) call the general antagonism, and with it, a new form of revolution. What would it be? A

detournement of financial processes and tools, a slow takeover of the economic operating system

occupying planet earth by those whose interests have been collapsed into bank interest. Indeed, it is the

incapacity to do just this granular and collective reformatting of the economy that has marked the

failure of previous revolutions. Thus far, beyond the initial desperation, beauty and romanticism of

revolutionary movements, we have mostly had various efforts at a seizing of the state that result in the

reintroduction and replication of the gendered, racial and hierarchical logics of capitalism. From the

Soviets, to the PRC, to scores of post-colonial states, we are familiar with the outcomes. The limitations

were both of imagination and technology; movements weighed down by default notions of centralization and

bureaucratic organization, notions that informed both emergent states and the discrete state computing that

would develop to run them and all the others. This time, with another century of struggle and know-how, if

we all listen to history and to the claims of the denizens of Earth, things may be different.

The ECSA project opens a spread on racial capitalism and endeavors to use its historically consolidated

capacities (our capacities), including the power of financial instruments and computing, to wager

on postcapitalist outcomes. Contrary to racial capitalism, the arbitrage on intelligence proposed here is to

reduce the cost to the planet for collective re-imagination and re-organization, while also collectivizing

the returns on the benefits of creating more convivial forms of life. We will reduce the price of survival,

in terms of violence to others, in terms of the individual requirements for the value-form (money), and in

absolute terms. Perhaps we will collectivize values creation and distribution/sharing to the point of

overcoming the value form of capital itself. In any case, by utilizing the accumulated knowledge implicit in

financial instruments and computing derived from, but not beholden to, capitalism, we will be creating a

grammar for postcapitalist economic expression. The ECSA vision might just open an option on postcapitalist

futures. This option would be one where we can risk together for non-capitalist outcomes, and do so from

within capital. As Jodi Melamed (2015:82) says:

Marx finds value itself to be a pharmekon: it is a poison because it is a measure of how much human labor

has been estranged and commodified by capital, yet it is also a medicine because it provides a way to

grasp individual human efforts as alienated social forces, which revolutionary struggles can turn toward

collective ends.

option if you would like to connect via mobile wallets.

option if you would like to connect via mobile wallets.